Page 169 - SUSTAINABILITY ISSUES & COVID-19

P. 169

From the results of the documentation obtained, the vision and mission of KAP X has reflected the existence of a

strategy or action that supports the achievement of quality by providing good service to clients and added value

to the client company. Based on the results of documentation and examination findings by IAPI, KAP X does not

have clear policies and procedures governing audit quality control. In fact, the manual for SPM KAP X still contains

several statements that are inconsistent with the nature and condition of the company. In addition, the existing

organizational structure does not describe the responsibilities of each KAP personnel. This certainly shows that the

assignment of work does not have a clear basis so it is difficult for KAP X to achieve company goals.

KAP X has a reward program aimed at employees who are able to bring or give new clients to KAP X. KAP X’s

colleagues support the program by always motivating and teaching employees how to get new clients. The reward

program is valid only for the achievement of the client, there is no reward program given to employees who excel in

the fields of quality, ethics, and discipline.

KAP X’s colleague appoints a senior staff to assist KAP X colleagues in developing, documenting, and supporting KAP

X’s SPM policies and procedures. There are no written policies and procedures regarding the assignment criteria.

4.1.2 Relevant Ethical Requirements

Public accountants have a responsibility for the public interest, this is the difference between the public accounting

profession and other professions. The basic principles of ethics for professional accountants are integrity, objectivity,

competence as well as due care and professional care, confidentiality and professional behavior. Ethics involves knowing

when to say “no” and when to cut off work with clients, staff, or even partners. By applying professional ethics, KAP can

create trust for report users, protect KAP from various ethical issues such as misstatement or misleading reports, fraud,

breaches of confidentiality, and others.

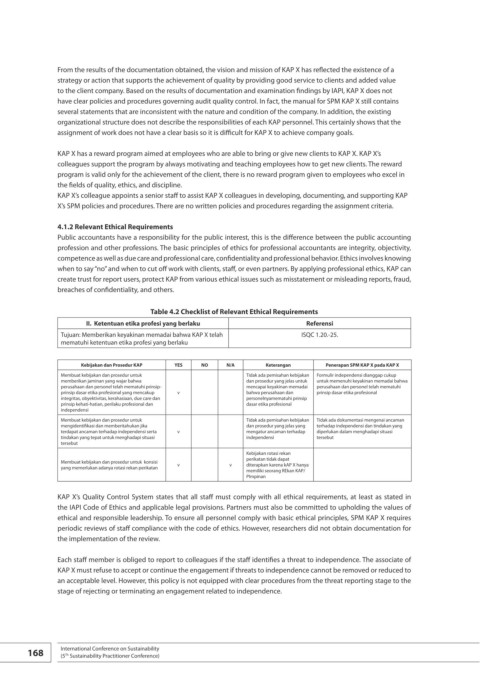

Table 4.2 Checklist of Relevant Ethical Requirements

II. Ketentuan etika profesi yang berlaku Referensi

Tujuan: Memberikan keyakinan memadai bahwa KAP X telah ISQC 1.20.-25.

mematuhi ketentuan etika profesi yang berlaku

Kebijakan dan Prosedur KAP YES NO N/A Keterangan Penerapan SPM KAP X pada KAP X

Membuat kebijakan dan prosedur untuk Tidak ada pemisahan kebijakan Formulir independensi dianggap cukup

memberikan jaminan yang wajar bahwa dan prosedur yang jelas untuk untuk memenuhi keyakinan memadai bahwa

perusahaan dan personel telah mematuhi prinsip- mencapai keyakinan memadai perusahaan dan personel telah mematuhi

prinsip dasar etika profesional yang mencakup v bahwa perusahaan dan prinsip dasar etika profesional

integritas, obyektivitas, kerahasiaan, due care dan personelnyamematuhi prinsip

prinsip kehati-hatian, perilaku profesional dan dasar etika profesional

independensi

Membuat kebijakan dan prosedur untuk Tidak ada pemisahan kebijakan Tidak ada dokumentasi mengenai ancaman

mengidentifikasi dan memberitahukan jika dan prosedur yang jelas yang terhadap independensi dan tindakan yang

terdapat ancaman terhadap independensi serta v mengatur ancaman terhadap diperlukan dalam menghadapi situasi

tindakan yang tepat untuk menghadapi situasi independensi tersebut

tersebut

Kebijakan rotasi rekan

perikatan tidak dapat

Membuat kebijakan dan prosedur untuk konsisi

yang memerlukan adanya rotasi rekan perikatan v v diterapkan karena kAP X hanya

memiliki seorang REkan KAP/

PImpinan

KAP X’s Quality Control System states that all staff must comply with all ethical requirements, at least as stated in

the IAPI Code of Ethics and applicable legal provisions. Partners must also be committed to upholding the values of

ethical and responsible leadership. To ensure all personnel comply with basic ethical principles, SPM KAP X requires

periodic reviews of staff compliance with the code of ethics. However, researchers did not obtain documentation for

the implementation of the review.

Each staff member is obliged to report to colleagues if the staff identifies a threat to independence. The associate of

KAP X must refuse to accept or continue the engagement if threats to independence cannot be removed or reduced to

an acceptable level. However, this policy is not equipped with clear procedures from the threat reporting stage to the

stage of rejecting or terminating an engagement related to independence.

168 International Conference on Sustainability

(5 Sustainability Practitioner Conference)

Th