Page 168 - SUSTAINABILITY ISSUES & COVID-19

P. 168

After carrying out the documentation process, the researcher found that KAP X did not have a special team or personnel

who were responsible for managing the regularity of company documentation both administratively and documents

related to KAP X’s quality control activities.

4. RESULT AND ANALYSIS

Based on the data obtained at the time of the research, the researcher gained an understanding of the process of

implementing the Quality Control System at KAP X. The researcher will discuss the results of this understanding and

then compare them with ISQC 1 implemented in Indonesia through SPM 1, analyze the findings obtained during the

study, and recommendations in the form of policies and procedures that need to be applied to the SPM KAP X. To

obtain a deep understanding and analyze problems regarding quality control at KAP X, researchers used three types

of approaches such as interviewing KAP X personnel, observation, and documentation. The following are the results

of the analysis that has been carried out:

4.1 Implementation of KAP X Quality Control System Compared to ISQC 1 Implemented

in Indonesia Through SPM 1

The researcher developed a checklist for audit quality control based on ISQC 1 and input from various standards.

Researchers also obtained input from the results of interviews conducted at KAP X regarding the expectations of KAP

X in improving audit quality. The findings that occur in the implementation of ISQC 1 can be considered by KAP X in

the future in monitoring the audit process.

ISQC 1 requires KAP to have an internal culture that prioritizes quality rather than commercial matters in carrying

out an engagement and assigns personnel who are responsible and have sufficient ability and experience to carry

out work. KAP is also asked to have adequate policies and procedures to support the quality or quality of the audit.

These policies and procedures must be in written form and their implementation documented so that they can be

accounted for. Meanwhile, the communication channels found in small KAP are shorter and simpler so that there is

minimal written documentation. Thus, the implementation of ISQC 1 in small KAP must be adjusted to the nature and

size of the company.

4.1.1 Leadership Responsibilities at Sole Proprietorship Public Accounting Firm

As stated in ISQC 1.18, company leadership and the examples implemented have a significant influence on the

company’s internal culture. In addition, the policies and procedures designed must also support an internal culture

with a commitment to prioritizing quality in carrying out an engagement. The internal culture of a KAP is reflected in

the vision, mission, policies and quality control procedures as a guideline for KAP in operating.

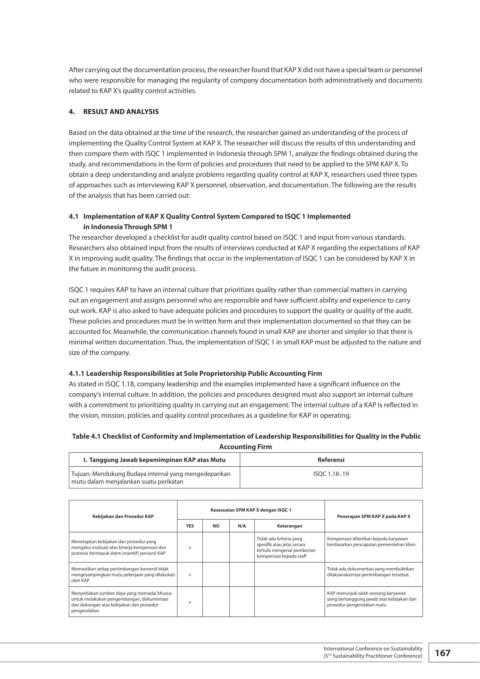

Table 4.1 Checklist of Conformity and Implementation of Leadership Responsibilities for Quality in the Public

Accounting Firm

I. Tanggung Jawab kepemimpinan KAP atas Mutu Referensi

Tujuan: Mendukung Budaya internal yang mengedepankan ISQC 1.18-.19

mutu dalam menjalankan suatu perikatan

Kesesuaian SPM KAP X dengan ISQC 1

Kebijakan dan Prosedur KAP Penerapan SPM KAP X pada KAP X

YES NO N/A Keterangan

Tidak ada kriteria yang Kompensasi diberikan kepada karyawan

Menetapkan kebijakan dan prosedur yang spesifik atau jelas secara berdasarkan pencapaian pemerolehan klien.

mengatur evaluasi atas kinerja kompensasi dan v

promosi (termasuk sitem insentif) personil KAP tertulis mengenai pemberian

kompensasi kepada staff

Memastikan setiap pertimbangan komersil tidak Tidak ada dokumentasi yang membuktikan

mengesampingkan mutu pekerjaan yang dilakukan v dilaksanakannya pertimbangan tersebut.

oleh KAP

Menyediakan sumber daya yang memadai khusus KAP menunjuk salah seorang karyawan

untuk melakukan pengembangan, dokumentasi yang bertanggung jawab atas kebijakan dan

dan dukungan atas kebijakan dan prosedur v prosedur pengendalian mutu

pengendalian

International Conference on Sustainability 167

(5 Sustainability Practitioner Conference)

Th