Page 38 - SUSTAINABILITY ISSUES & COVID-19

P. 38

The correct and adequate implementation of the state-owned asset revaluation will increase public confidence and

interested parties in government financial reports so that they can make the right economic decisions. This study aims

to explore and find out the main problems that occur in the implementation of the state-owned asset revaluation. The

hope is that the studies can find a description of the main problem in implementing the state-owned asset revaluation.

The benefits obtained are in the form of proposed improvements to the process of implementing the state-owned

asset revaluation in the future. It can also be a reference if the local government will carry out the Region-owned

asset revaluation. This research expectation is to contribute knowledge in government accounting in the field of asset

management, especially related to asset revaluation.

2. LITERATURE REVIEW

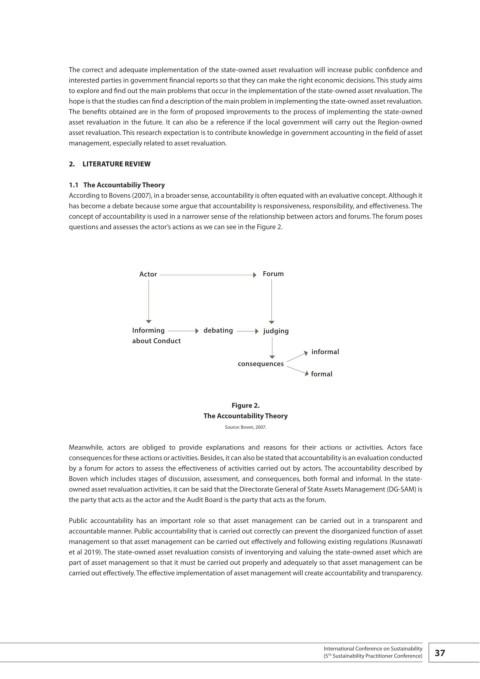

1.1 The Accountabiliy Theory

According to Bovens (2007), in a broader sense, accountability is often equated with an evaluative concept. Although it

has become a debate because some argue that accountability is responsiveness, responsibility, and effectiveness. The

concept of accountability is used in a narrower sense of the relationship between actors and forums. The forum poses

questions and assesses the actor’s actions as we can see in the Figure 2.

Actor Forum

Informing debating judging

about Conduct

informal

consequences

formal

Figure 2.

The Accountability Theory

Source: Boven, 2007.

Meanwhile, actors are obliged to provide explanations and reasons for their actions or activities. Actors face

consequences for these actions or activities. Besides, it can also be stated that accountability is an evaluation conducted

by a forum for actors to assess the effectiveness of activities carried out by actors. The accountability described by

Boven which includes stages of discussion, assessment, and consequences, both formal and informal. In the state-

owned asset revaluation activities, it can be said that the Directorate General of State Assets Management (DG-SAM) is

the party that acts as the actor and the Audit Board is the party that acts as the forum.

Public accountability has an important role so that asset management can be carried out in a transparent and

accountable manner. Public accountability that is carried out correctly can prevent the disorganized function of asset

management so that asset management can be carried out effectively and following existing regulations (Kusnawati

et al 2019). The state-owned asset revaluation consists of inventorying and valuing the state-owned asset which are

part of asset management so that it must be carried out properly and adequately so that asset management can be

carried out effectively. The effective implementation of asset management will create accountability and transparency.

International Conference on Sustainability 37

(5 Sustainability Practitioner Conference)

Th