Page 44 - SUSTAINABILITY ISSUES & COVID-19

P. 44

owned asset and local-owned asset. Those who have the authority and responsibility for the results of the inventory

are the ministries/government agencies existing as the Asset User of Proxy. His job is to carry out an inventory, compile

a report on the results of the inventory then follow up on findings that occur during the inventory. Then the results of

the inventory will be matched and clarified by the Asset Manager/DG-SAM. For comparison, between the inventory in

the state-owned asset activity and the inventory held every five years, the inventory in the revaluation activity should

have no problem. However, in reality, there are still many problems related to inventory when the state-owned asset

revaluation is implemented in 2017-2018. This proves that the inventory in the ministries/government agencies is still

not implemented adequately due to the different policies implemented by each ministries/government agencies in

carrying out the five-year inventory.

There are weaknesses in the implementation of the Inventory, namely: In the implementation of the inventory there

are still many implementation teams at the ministries/government agencies that do not understand their duties, many

items are not managed properly so that their whereabouts are often unknown. Before the implementation of the

inventory and re-evaluation activities, the DG-SAM has conducted socialization to the Aset User intending to expedite

inventory activities. However, in practice there are still many officers who do not understand their duties, this can affect

the quality of the inventory results. According to Sangadji (2018), the quality of inventory implementation affects legal

audits and asset valuations. The poor quality of the inventory results will affect the reliability of the fair value of the

state-owned asset revaluation results.

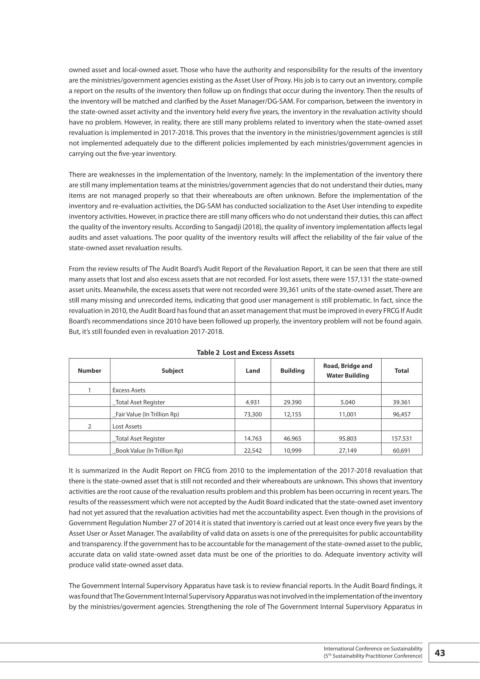

From the review results of The Audit Board’s Audit Report of the Revaluation Report, it can be seen that there are still

many assets that lost and also excess assets that are not recorded. For lost assets, there were 157,131 the state-owned

asset units. Meanwhile, the excess assets that were not recorded were 39,361 units of the state-owned asset. There are

still many missing and unrecorded items, indicating that good user management is still problematic. In fact, since the

revaluation in 2010, the Audit Board has found that an asset management that must be improved in every FRCG If Audit

Board’s recommendations since 2010 have been followed up properly, the inventory problem will not be found again.

But, it’s still founded even in revaluation 2017-2018.

Table 2 Lost and Excess Assets

Road, Bridge and

Number Subject Land Building Total

Water Building

1 Excess Asets

_Total Aset Register 4.931 29.390 5.040 39.361

_Fair Value (In Trillion Rp) 73,300 12,155 11,001 96,457

2 Lost Assets

_Total Aset Register 14.763 46.965 95.803 157.531

_Book Value (In Trillion Rp) 22,542 10,999 27,149 60,691

It is summarized in the Audit Report on FRCG from 2010 to the implementation of the 2017-2018 revaluation that

there is the state-owned asset that is still not recorded and their whereabouts are unknown. This shows that inventory

activities are the root cause of the revaluation results problem and this problem has been occurring in recent years. The

results of the reassessment which were not accepted by the Audit Board indicated that the state-owned aset inventory

had not yet assured that the revaluation activities had met the accountability aspect. Even though in the provisions of

Government Regulation Number 27 of 2014 it is stated that inventory is carried out at least once every five years by the

Asset User or Asset Manager. The availability of valid data on assets is one of the prerequisites for public accountability

and transparency. If the government has to be accountable for the management of the state-owned asset to the public,

accurate data on valid state-owned asset data must be one of the priorities to do. Adequate inventory activity will

produce valid state-owned asset data.

The Government Internal Supervisory Apparatus have task is to review financial reports. In the Audit Board findings, it

was found that The Government Internal Supervisory Apparatus was not involved in the implementation of the inventory

by the ministries/goverment agencies. Strengthening the role of The Government Internal Supervisory Apparatus in

International Conference on Sustainability 43

(5 Sustainability Practitioner Conference)

Th