Page 180 - SUSTAINABILITY ISSUES & COVID-19

P. 180

schemes, bribery, gratuities, extortion. According to the CPA guidelines for fraud and commercial crime prevention,

employees should not accept gifts, preferential treatment in any way that could influence or appear to influence

business decisions with a person or organization, thereby reducing their liability.

2. Asset Misappropriation

Asset misappropriation can be divided into theft of cash or company deposits, taking cash transactions and officially

reporting a lower revenue volume, theft through unauthorized expenses through some intermediary.

3. Financial Statement Fraud

Engineering corporate financial statements for personal gain.

Bribery is an example of fraud, so this study chooses the Fraud Triangle Theory approach to answer how business

barriers affect bribery. Initially this theoretical concept was used to understand financial crime. According to the

Fraud Triangle Theory, there are 3 elements in the occurrence of fraud, namely pressure / incentive (pressure),

opportunity (opportunity), and rationalization (rationalization).

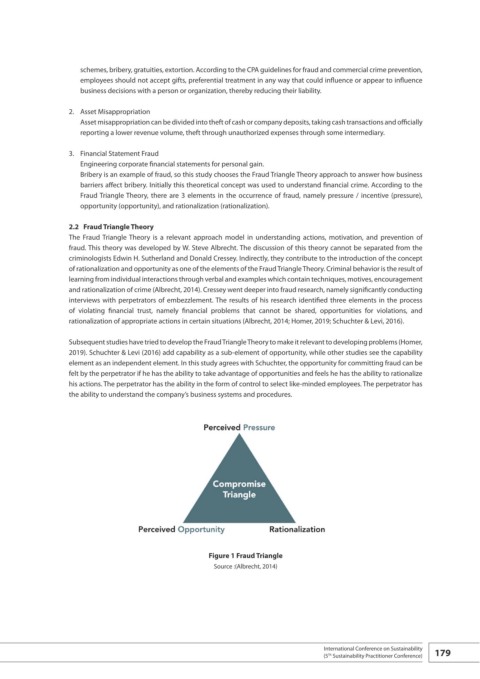

2.2 Fraud Triangle Theory

The Fraud Triangle Theory is a relevant approach model in understanding actions, motivation, and prevention of

fraud. This theory was developed by W. Steve Albrecht. The discussion of this theory cannot be separated from the

criminologists Edwin H. Sutherland and Donald Cressey. Indirectly, they contribute to the introduction of the concept

of rationalization and opportunity as one of the elements of the Fraud Triangle Theory. Criminal behavior is the result of

learning from individual interactions through verbal and examples which contain techniques, motives, encouragement

and rationalization of crime (Albrecht, 2014). Cressey went deeper into fraud research, namely significantly conducting

interviews with perpetrators of embezzlement. The results of his research identified three elements in the process

of violating financial trust, namely financial problems that cannot be shared, opportunities for violations, and

rationalization of appropriate actions in certain situations (Albrecht, 2014; Homer, 2019; Schuchter & Levi, 2016).

Subsequent studies have tried to develop the Fraud Triangle Theory to make it relevant to developing problems (Homer,

2019). Schuchter & Levi (2016) add capability as a sub-element of opportunity, while other studies see the capability

element as an independent element. In this study agrees with Schuchter, the opportunity for committing fraud can be

felt by the perpetrator if he has the ability to take advantage of opportunities and feels he has the ability to rationalize

his actions. The perpetrator has the ability in the form of control to select like-minded employees. The perpetrator has

the ability to understand the company’s business systems and procedures.

Figure 1 Fraud Triangle

Source :(Albrecht, 2014)

International Conference on Sustainability 179

(5 Sustainability Practitioner Conference)

Th